The Terrifying Shadow of Inflation: Why It Still Haunts Global Economies in 2026

In 2026, stubborn global inflation—driven by supply bottlenecks, energy shocks from Middle East tensions, tariffs, and geopolitical instability—continues dominating economic debates, squeezing households and challenging central banks’ rate strategies.

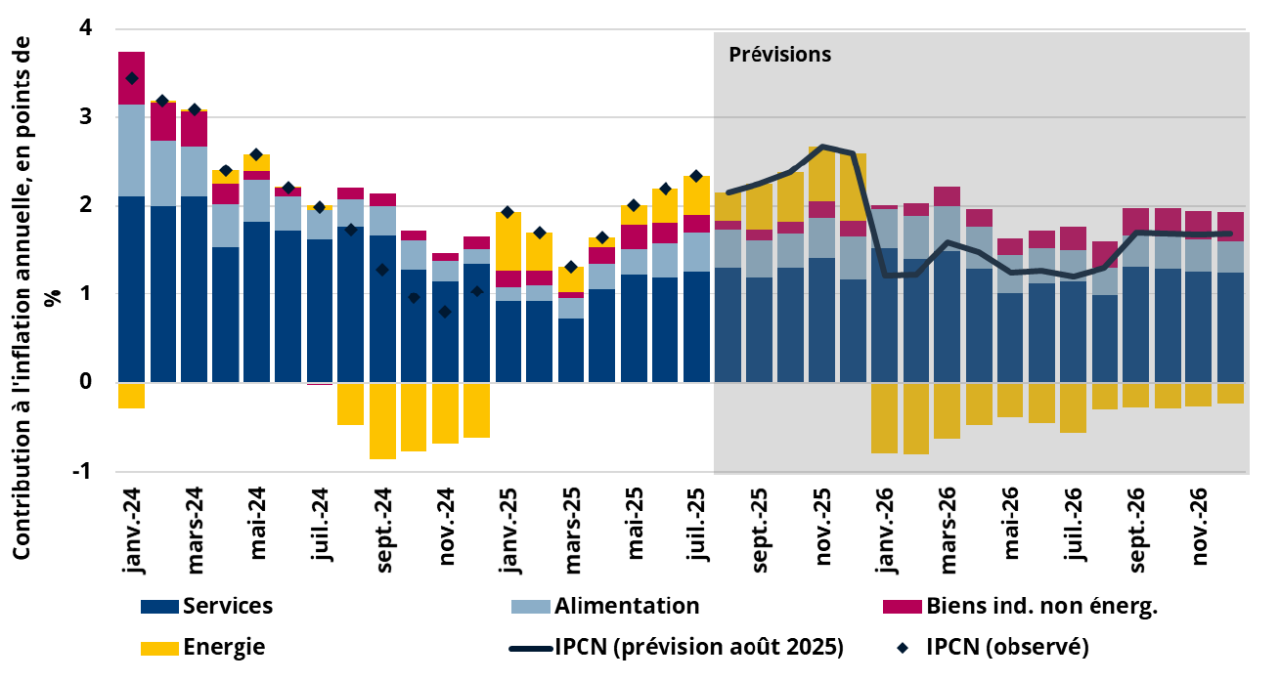

In March 2026, as geopolitical tensions in the Middle East escalate and oil prices surge by over 20%, global inflation 2026 refuses to fade into the background, commanding center stage in economic discussions worldwide. Far from the transient spike seen in previous years, inflation’s stubborn persistence above central bank targets hovering around 2.8% for global core measures, signals deeper structural challenges that threaten sustained growth and stability. Policymakers, businesses, and households are grappling with rising costs that erode purchasing power, while forecasts project global headline inflation at approximately 3.1% to 3.7% for the year, underscoring why this economic force continues to shape fiscal strategies, investment decisions, and everyday lives across continents.

This enduring concern stems from a confluence of factors that have evolved since the post-pandemic recovery. While initial surges were tied to supply shocks and demand rebounds, persistent inflation 2026 narrative is marked by intertwined global disruptions that amplify price pressures. Economists at institutions like J.P. Morgan and the IMF highlight how regional divergences, such as U.S. inflation accelerating to over 3% while Europe moderates toward 2% complicate unified responses. As central banks navigate this landscape, the debate intensifies: Can traditional tools like interest rate adjustments finally rein in inflation, or will new vulnerabilities prolong the battle?

Supply Chain Disruptions: The Enduring Bottleneck Driving Up Costs in 2026

Supply chain pressures remain a primary culprit behind persistent inflation, with disruptions originating from the pandemic era now compounded by trade wars and logistical hurdles. In 2026, global logistics indices show a modest uptick in stress levels, driven by rerouting around conflict zones like the Red Sea and escalating shipping costs amid U.S. tariffs. These bottlenecks have led to delayed deliveries and higher freight rates, which businesses pass on to consumers through elevated goods prices.

Research from the Cleveland Fed indicates that supply chain issues contributed significantly to inflation’s rise since 2021, accounting for a substantial portion of price increases in core categories. For instance, non-energy industrial goods in the euro area saw monthly rises of 0.7% in early 2026, reflecting ongoing constraints. EY’s outlook notes that while some easing occurred in 2025, persistent tariffs and inventory drawdowns have reversed gains, pushing import costs higher and sustaining inflationary momentum.

This dynamic is particularly evident in manufacturing, where input shortages amplify costs. The ISM’s price sub-index jumped to 70.5 in early 2026, its highest since mid-2022, signaling renewed pressures that could filter into consumer prices over months. As global trade flows adjust slowly, these disruptions underscore inflation’s resilience, forcing economies to contend with higher baseline costs.

Surging Energy Costs: Geopolitical Tensions Fuel Inflation Fears Worldwide

Energy prices have emerged as a volatile driver of inflation in 2026, exacerbated by Middle Eastern conflicts that disrupt key supply routes. Brent crude oil surged 28% amid Iran’s involvement and Qatar’s export halts through the Strait of Hormuz, a chokepoint for one-fifth of global oil. This has cascading effects, with European electricity prices rising 31% and natural gas wholesales jumping nearly 50% in early March.

Goldman Sachs estimates that a sustained 10% oil price increase boosts consumer price indices by 0.28 percentage points, highlighting energy’s role in headline inflation. In the U.S., energy components have contributed to sticky inflation around 3%, while Europe’s headline rate ticked up to 1.9% in February, partly due to these shocks. The IMF warns that prolonged conflicts could spike inflation further through commodity market speculation and supply curtailments.

These costs extend beyond fuel, influencing transportation and production expenses across sectors. As energy inflation feeds into core measures, it challenges the narrative of transitory pressures, making 2026 a pivotal year for energy-dependent economies.

Geopolitical Instability: Wars and Tariffs Sustain Global Price Pressures

Geopolitical risks have intensified inflation’s grip, with ongoing conflicts and trade policies creating uncertainty that elevates costs. The Russia-Ukraine war’s legacy, combined with Middle East escalations, has curtailed supplies of commodities like grains and metals, pushing food inflation to a global average of 3.2%.

U.S. tariffs, implemented broadly in late 2025, have added 0.5 to 0.75 percentage points to current inflation rates, with pass-through to consumers exceeding 50%. Brookings experts note that persistent high tariffs could shift trade dynamics, raising import prices and contributing to a 1% inflation uplift in early 2026. In emerging markets, collective inflation stands at 5.2%, reflecting amplified vulnerabilities.

This instability fosters a risk-averse environment, where businesses hoard inventories and investors demand higher premiums, further entrenching inflationary trends.

Central Bank Policies: Navigating the Tightrope of Inflation Control

Central banks’ responses to past inflation surges through aggressive rate hikes, have shaped the current landscape, but their effectiveness in 2026 remains under scrutiny. The synchronized global tightening prevented de-anchoring of expectations, yet sticky core inflation persists due to labor constraints and fiscal stimuli.

In the U.S., fiscal dominance from high debt limits the Fed’s flexibility, with deficits nearing 7% of GDP amplifying price pressures. European and Asian policies show bifurcation, with some easing amid sub-2% inflation. Overall, these policies have moderated demand but struggle against supply-side shocks.

Inflation’s Squeeze on Households: Everyday Costs Erode Purchasing Power

Households worldwide face acute pressures from inflation, with U.S. consumer prices rising 2.4% year-over-year in January, driven by rents and food. Lower-income families, spending more on necessities, bear the brunt, as affordability crises deepen amid stagnant wages relative to costs.

In Europe, food price hikes influence perceptions and wage negotiations, while global trends show consumers economizing. Savings rates dwindle, exacerbating vulnerability to shocks.

Businesses Battle Rising Costs: Margins Tighten Amid Inflation Woes

Small businesses adapt by increasing marketing spend, yet face higher inputs and reduced consumer demand. Tariffs and energy costs compress profits, with many passing increases to customers, risking sales drops.

Larger firms leverage AI investments for efficiency, but overall, inflation hampers growth and innovation.

Governments Grapple with Fiscal Strain: Inflation Amplifies Debt Challenges

Governments contend with elevated debt servicing, as U.S. federal spending dropped 16.6% in Q4 2025, shaving GDP growth. Reduced revenues and higher borrowing costs limit policy responses, while shutdowns delay reimbursements.

Globally, fiscal paths risk crowding out private investment, with debt nearing 120% of GDP in advanced economies.

Central Banks’ Interest Rate Strategies: Responding to Persistent Inflation

Central banks maintain cautious stances, with the Fed holding at 3.5-3.75% in January, eyeing cuts if inflation eases. The ECB and BoE show splits, prepared for hikes amid energy shocks.

Data-driven approaches balance employment and price stability, with gradual easing projected.

Assessing Effectiveness: Can Rate Policies Succeed in Taming Inflation?

Interest rate policies have stabilized expectations but face limits against supply shocks, with effectiveness tempered by geopolitical risks. Fed projections see inflation nearing 2% by 2027, yet upside risks persist. Balanced views suggest success hinges on resolving external pressures, with communication aiding credibility.

In summary, while tools like rate adjustments provide leverage, broader reforms are needed for lasting relief.