The Reality Behind the Trustee Bank Account Strategy

The idea that you should “never open a bank account in your name” sounds powerful. But is it legally sound? This complete guide to the trustee bank account strategy will explain how trust accounts work, their genuine benefits, hidden dangers and if they truly protect your financial assets.

The claim that you should never open a saving bank account under your own name carries an air of exclusivity, as though it is a hidden financial loophole used by the wealthy or legally savvy. At its core, however, this idea is simply a reinterpretation of how trust structures work within modern banking systems. What is often marketed as a secret tactic is, in reality, a formal and regulated legal arrangement that has existed for centuries.

A trust account does not make money disappear from legal oversight. Instead, it reassigns ownership into a structured relationship governed by law. When assets are placed into a trust, they are no longer held in a straightforward personal capacity but are instead managed according to rules defined in a legal document. This shift creates the impression of distance between the individual and the funds, but that distance is conditional, not absolute. The law still recognizes the connection, especially when the structure is revocable or when the original owner retains control.

Trustee Bank Account Strategy: How It Actually Works

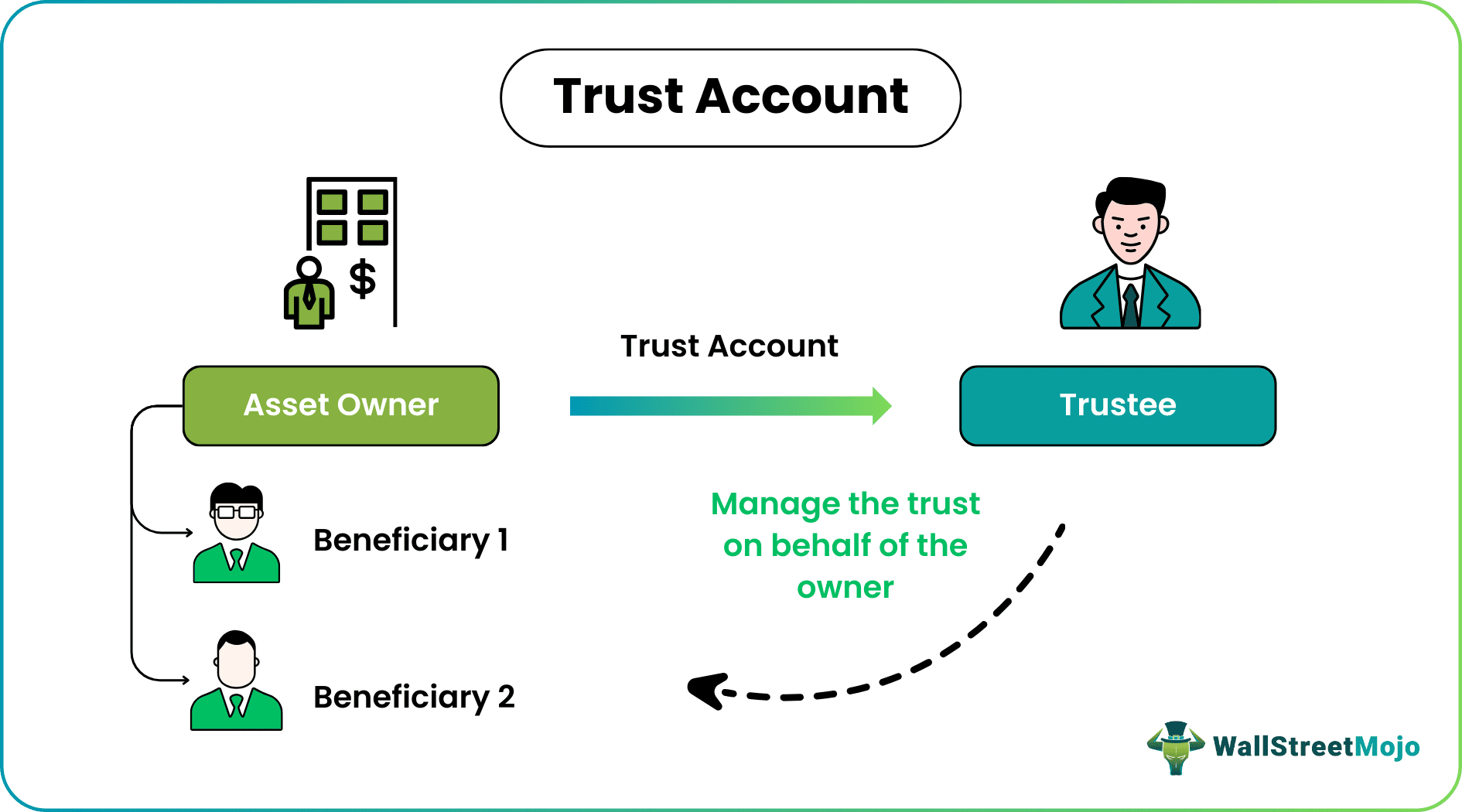

To understand the trustee bank account strategy, it is necessary to examine the legal architecture behind a trust. A trust is built on a relationship involving a creator, a manager, and a beneficiary. The creator, often called the grantor, establishes the trust and transfers assets into it. The trustee becomes responsible for managing those assets, while the beneficiary is the party intended to benefit from them.

What makes this structure distinct is the separation between legal control and beneficial interest. The trustee holds legal authority over the account, but that authority is limited by the instructions contained in the trust agreement. This creates a system where control is exercised within strict boundaries rather than freely, as would be the case with a personal bank account.

This distinction is where many misconceptions arise. Simply opening an account under another person’s name does not constitute a trust arrangement. Without a formal trust document and legal recognition, the account remains subject to ordinary ownership rules, which means the supposed protections do not exist.

Revocable Trust Account Setup: Control vs Ownership

The concept of a revocable trust account is central to this strategy because it offers flexibility. A revocable trust allows the person who created it to amend or dissolve it at any time, which creates a sense of retained control. In many cases, individuals choose to act as both the creator and the trustee, effectively maintaining day-to-day authority over the assets.

This arrangement gives rise to the belief that one can separate ownership while still exercising full control. In practice, however, the law views revocable trusts differently from irrevocable ones. Because the creator can reverse the arrangement at will, the assets are still closely tied to that individual. This means that, for purposes such as taxation, debt recovery, or legal enforcement, the trust may not provide meaningful separation.

The tension between control and ownership is therefore not resolved by a revocable trust; it is merely reframed. The individual gains administrative flexibility but does not escape legal responsibility.

Asset Protection Trust Accounts: Myth vs Reality

Much of the appeal surrounding the trustee bank account strategy is rooted in the promise of asset protection. The narrative suggests that once funds are placed in a trust, they become shielded from external threats such as creditors or legal authorities. While there is some basis for this belief, it is often exaggerated beyond what the law actually allows.

Trusts can provide a degree of protection, particularly when they are structured as irrevocable arrangements where the creator relinquishes control. In such cases, the assets are no longer considered part of the individual’s personal estate. However, this comes at a cost, as the individual must genuinely give up access and authority over those funds.

In contrast, revocable trusts offer minimal protection because the connection between the individual and the assets remains intact. Courts can look through the structure and treat the assets as belonging to the creator when necessary. This means that the idea of a trust as an impenetrable shield is more myth than reality, especially in commonly used setups.

Legal Bank Account Freezing: What Really Happens

The belief that a trust account cannot be frozen is one of the most misleading aspects of this strategy. In reality, financial institutions operate under legal frameworks that apply to all accounts, regardless of their structure. When authorities have a lawful basis to intervene, they can act on both personal and trust accounts.

Account freezing typically occurs under specific conditions, such as court orders, regulatory investigations, or enforcement of debts. In the context of a trust, the legal process may involve directing orders toward the trustee, who is responsible for managing the account. The existence of a trust does not prevent this process; it simply changes the procedural pathway.

This means that while a trust can introduce additional layers of administration, it does not remove the possibility of legal intervention. The notion that funds become untouchable once placed in a trustee’s name is therefore inaccurate and potentially dangerous if relied upon without proper understanding.

How to Open a Trust Account Properly

Establishing a trust account requires more than a simple visit to a bank. The process begins with the creation of a legally valid trust document, which outlines the terms under which the assets will be managed. This document serves as the foundation of the entire structure, defining roles, responsibilities, and limitations.

Once the trust is established, a bank account can be opened in its name. The financial institution will typically require verification of the trust’s existence, identification of the trustee, and compliance with regulatory requirements such as tax reporting. The account is then operated by the trustee in accordance with the trust agreement.

This process underscores an important point: legitimacy is essential. Without proper documentation and compliance, the account will not be recognized as a trust account, and any perceived benefits will not apply. The structure must align with legal standards to function as intended.

Trustee and Guarantor Structure: Who Really Has Power?

The idea of combining roles such as trustee and guarantor often leads to confusion about who truly holds power within the arrangement. In a trust, authority is derived from the role of the trustee, who is legally obligated to act in the best interests of the beneficiaries and within the confines of the trust document.

A guarantor, on the other hand, typically assumes responsibility for obligations rather than control over assets. This distinction is critical because it highlights the limits of influence that different roles carry. If an individual is not the trustee, their ability to direct the account is significantly constrained.

Even when the same person occupies multiple roles, their actions are still governed by legal duties. The trust structure does not grant unlimited freedom; it imposes a framework within which decisions must be made. This ensures accountability but also limits the extent to which the arrangement can be manipulated for personal advantage.

Benefits of Trustee Bank Account Strategy

When applied correctly, the Trustee Bank Account Strategy offers meaningful advantages. One of its most significant strengths lies in its ability to facilitate estate planning. By placing assets in a trust, individuals can ensure a smoother transfer of wealth, avoiding the delays and public exposure associated with probate processes.

The structure also provides continuity in asset management. If the creator becomes incapacitated, the trustee can continue to manage the funds without interruption, preserving stability for beneficiaries. This makes trust accounts particularly valuable in long-term financial planning.

Privacy is another notable benefit. While not absolute, the use of a trust can reduce the visibility of financial arrangements compared to standard ownership models. This can be appealing for individuals who prioritize discretion in their financial affairs.

Trust Account Benefits and Risks: A Balanced View

Despite these advantages, trust accounts are not without their drawbacks. One of the primary concerns is the potential loss of direct control, especially when an independent trustee is involved. This introduces an element of reliance that may not suit all individuals.

There are also financial and administrative costs associated with setting up and maintaining a trust. Legal fees, compliance requirements, and ongoing management can make the structure more complex than a traditional bank account.

Additionally, the level of protection offered by a trust depends heavily on how it is structured. Misunderstanding this aspect can lead to misplaced confidence and, in some cases, legal complications. The balance between benefits and risks must therefore be carefully evaluated before adopting this strategy.

Is the Trustee Bank Account Strategy a Good Move?

Determining whether this strategy is a good move requires clarity of purpose. For individuals seeking structured wealth management, estate planning, or continuity in financial oversight, a trust account can be an effective tool. It provides a framework that aligns with long-term planning objectives and offers a degree of organization that personal accounts cannot match.

However, for those motivated by the desire to evade scrutiny or avoid legal obligations, the strategy is fundamentally flawed. Trusts operate within the same legal systems as personal accounts, and attempts to misuse them can lead to serious consequences.

The key lies in understanding that a trust is not a loophole but a legal instrument. Its value depends on how it is used and whether it aligns with legitimate financial goals.

Final Analysis: Control, Illusion, and Smart Strategy

The trustee bank account strategy sits at the intersection of genuine financial planning and widespread misconception. It offers real benefits when used appropriately, but it also carries risks when misunderstood or misapplied.

The idea that one should never open a saving bank account under their own name is not inherently sound advice. Personal accounts remain essential for everyday financial activities, while trust accounts serve more specialized purposes. The two are not mutually exclusive but complementary.

Ultimately, the effectiveness of this strategy depends on informed decision-making. By recognizing both its strengths and its limitations, individuals can avoid the pitfalls of illusion and make choices that genuinely enhance their financial security. Read also