How Middle East Tensions Could Shake the Global Economy and Energy Markets

As Iran-Israel-U.S. clashes shut the Strait of Hormuz, oil prices spike and global LNG flows stall. The 2026 Middle East crisis threatens to unleash inflation, supply shocks, and economic slowdown—echoing the oil crises of 1973 and 1990 on a modern, interconnected scale.

The Escalating Conflict in the Middle East: What You Need to Know

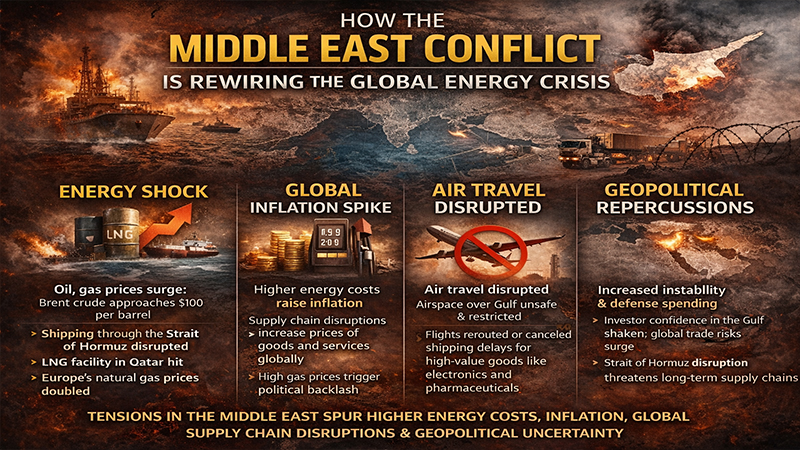

The Middle East Tensions has long been a flashpoint for geopolitical tensions, but the events unfolding in early 2026 have elevated risks to a new level. On February 28, 2026, the United States and Israel launched coordinated strikes on Iranian targets, including military facilities in Tehran, Isfahan, and Qom. Iran responded with missile attacks on U.S. and Israeli positions, as well as strikes on energy infrastructure in neighboring countries like Qatar and Saudi Arabia. This escalation has led to the effective closure of the Strait of Hormuz, a narrow waterway between Iran and Oman that serves as a vital artery for global energy trade.

The conflict stems from longstanding rivalries, including Iran’s support for proxy groups like Hezbollah and the Houthis, and accusations of nuclear program violations. Historical context reveals patterns: the 1973 Yom Kippur War triggered an Arab oil embargo, causing prices to quadruple and sparking global recessions. Similarly, the 1979 Iranian Revolution led to supply disruptions that doubled oil prices. Today, with Iran producing about 3.2 million barrels per day (bpd) of oil, around 3% of global output, the immediate focus is on transit routes rather than production losses.

As of March 8, 2026, over 200 vessels, including oil tankers and liquefied natural gas (LNG) carriers, remain anchored outside the Strait, unable to pass due to heightened war risks and insurance cancellations. This has already caused Brent crude prices to surge 13% to above $82 per barrel, the highest since July 2024. European natural gas futures jumped more than 40% following Qatar’s production halt at its Ras Laffan facility. The global significance lies in the region’s role: the Middle East accounts for about 30% of world oil supply and a substantial share of LNG exports. Disruptions here threaten energy security for import-dependent economies in Europe and Asia, potentially exacerbating inflation and slowing growth worldwide.

Historical Echoes: Lessons from Past Oil Crises

Past Middle East Tensions provide a blueprint for understanding current risks. The 1973 oil crisis, triggered by the Yom Kippur War, saw OPEC nations embargo oil exports to the U.S. and allies, reducing global supply by 5% and causing prices to rise from $3 to $12 per barrel. This led to stagflation in major economies: U.S. GDP contracted by 2.6% in 1974, while inflation hit 11%. Europe faced similar challenges, with energy rationing and industrial slowdowns.

The 1990-1991 Gulf War offers another parallel. Iraq’s invasion of Kuwait removed 4.3 million bpd from the market, pushing prices from $17 to $40 per barrel. Global growth slowed to 1.9% in 1991, down from 3.1% the prior year, according to World Bank data. However, strategic petroleum reserves and increased production from Saudi Arabia mitigated the worst effects, limiting the recession’s depth.

In 2019, drone attacks on Saudi Arabia’s Abqaiq facility halved the kingdom’s output temporarily, causing a 20% price spike. Markets recovered quickly due to ample global spares, but it highlighted vulnerabilities in processing infrastructure. Today’s situation differs: buffers like U.S. shale production (13 million bpd) and OPEC+ spare capacity (about 5 million bpd) exist, but a prolonged Strait closure could overwhelm them. Analysts note that while direct GDP impact from Gulf economies (2-3% of global output) is limited, energy transmission channels amplify effects. A sustained $10 oil price increase typically adds 0.2-0.3 percentage points to global inflation within six to twelve months, per IMF estimates. These historical lessons underscore that short disruptions are manageable, but extended conflicts risk broader economic fallout.

Current Developments: Strikes, Disruptions, and Price Surges

The conflict intensified rapidly. U.S. and Israeli airstrikes targeted Iranian leadership, including reports of Supreme Leader Ali Khamenei’s death, prompting Iranian retaliation against U.S. bases in the region and energy sites in Qatar and Saudi Arabia. QatarEnergy declared force majeure on LNG shipments after a drone strike on its facilities, halting output from the world’s second-largest exporter.

Saudi Arabia shuttered its Ras Tanura refinery following a drone attack, reducing domestic refining capacity. Iran temporarily closed parts of the Strait for “military drills” in mid-February, but the current shutdown stems from active hostilities, with at least four tankers damaged and one seafarer killed. Shipping data shows 150-200 vessels idled, disrupting 20% of global seaborne oil and LNG flows.

Oil prices reacted sharply: Brent crude rose 8-13% in early March trading, settling around $79-82 per barrel. U.S. West Texas Intermediate climbed to $72.40. Gasoline prices in the U.S. hit $3 nationwide, up 12 cents weekly, with analysts forecasting further increases. European gas prices surged 40-70%, reflecting Qatar’s 20% share of global LNG. Equity markets tumbled: the Nikkei and Hang Seng fell sharply, while U.S. stocks dipped amid $100 oil fears. These developments highlight immediate supply chain strains, with freight rates doubling and tanker costs reaching records.

The Strait of Hormuz: The World’s Most Critical Energy Chokepoint

The Strait of Hormuz, a 24-mile-wide passage at its narrowest, handles about 21 million bpd of oil—20% of global consumption—and 20% of LNG trade. Flanked by Iran and Oman, it’s the only sea route from the Persian Gulf to open oceans, making it indispensable for exporters like Saudi Arabia (7 million bpd), Iraq (3.5 million), UAE (2.5 million), and Kuwait (2 million).

Iran’s control over one side allows it to threaten closures, as seen in past drills and current conflict. Alternatives are limited: Saudi Arabia’s East-West Pipeline can reroute 5 million bpd to the Red Sea, but at reduced efficiency. UAE’s Fujairah bypass handles only 1.5 million bpd. Qatar and Iraq lack viable options, risking full export halts.

Disruptions here have global repercussions. A 10-14 day buffer exists via strategic reserves, but prolonged blockages could cut supply by 15-20%, per energy analysts. This chokepoint also carries petrochemicals, fertilizers, and helium—Qatar supplies 40% of global helium, critical for semiconductors. The Strait’s vulnerability underscores why even temporary closures drive volatility, affecting everything from fuel prices to manufacturing costs worldwide.

Impact on Global Oil Prices: Why $100 Oil Could Be Next

Oil prices have already climbed 12-14% since the conflict’s onset, with Brent peaking at $82. Analysts project further rises: Goldman Sachs sees $80-90, while JPMorgan’s worst-case is $120-130 if disruptions persist. Allianz forecasts $100 in a three-month scenario, potentially $130 if infrastructure is targeted.

The surge stems from supply fears rather than actual scarcity so far. Global demand is 103 million bpd, with Middle East exports at 30%. A full Strait closure could remove 15-20 million bpd initially, though reroutes might mitigate half. U.S. gasoline prices rose to $3.45, the highest since September 2024, with $4 possible.

Higher prices benefit non-Gulf exporters: U.S. shale could ramp up, Russia gains from premiums. But importers suffer: China and India, reliant on Gulf oil, face wider deficits and currency pressures. Every $10 increase adds 0.1-0.2 percentage points to short-term inflation in the U.S. and Europe, per Allianz. If prices stabilize at $70 by year-end, impacts remain contained; otherwise, $100 oil risks renewed stagflation.

Natural Gas and LNG Markets Under Pressure

LNG markets are equally strained. Qatar, producing 77 million tons annually (20% of global supply), halted exports after strikes, spiking European prices 40-70%. UAE and Iran add to disruptions, with 20% of LNG transiting the Strait.

Europe, post-Russia pivot, relies on Qatar for 15% of imports. Prices hit levels not seen since 2022’s Ukraine crisis, threatening energy security amid winter demand. Asia, including Japan and South Korea, faces similar risks, with freight rates surging.

U.S. and Australian producers benefit, but global tightness persists. A prolonged halt could reduce LNG supply by 15-20%, pushing prices higher and forcing rationing in import-dependent regions. This compounds oil effects, raising power generation costs and industrial expenses worldwide.

Broader Economic Implications: Inflation, Growth, and Central Banks

The conflict tests global resilience. IMF’s Dan Katz notes potential impacts on inflation and growth, with prolonged high energy prices delaying rate cuts. A 10% oil rise adds 0.1-0.2pp to inflation, per estimates.

Global GDP could slow: Allianz sees contained effects if short-lived, but three months as a turning point for recession risks. Emerging markets are vulnerable, with higher import bills and currency depreciation.

Central banks face dilemmas: Fed and ECB might hold rates, with U.S. 10-year yields drifting to 4.3%. Equity corrections of 20% possible in tail risks, while sectors like defense and energy gain. Supply chains suffer: shipping costs up, affecting goods from semiconductors to fertilizers.

Vulnerable Regions: Europe, Asia, and Emerging Markets

Europe and Asia bear the brunt. Europe, importing 40% of gas from the region, risks renewed crises. Asia’s China and India face deficits, with India potentially gaining manufacturing share from China.

Emerging markets like Pakistan see oil import costs rise, pressuring currencies. Gulf states benefit short-term but face instability.

Expert Insights: What Analysts Are Saying

IMF’s Kristalina Georgieva warns of “new shocks” testing resilience. Chatham House notes limited GDP impact but energy risks. BlackRock views it as a volatility shock. Wood Mackenzie predicts higher LNG prices.

Potential Scenarios: From Short-Term Shock to Prolonged Crisis

Base case (60%): Short conflict, oil at $70 by year-end. Bull (25%): Quick resolution, prices drop. Bear (15%): Escalation to $130, recession.

Why This Matters for the Global Future: A Call for Resilience

The 2026 Middle East conflict underscores energy interdependence and geopolitical fragility. Short-term, it risks inflation and slowdowns; long-term, it accelerates diversification toward renewables and alternative routes. Global growth could dip 1-2% if prolonged, per IEA-aligned studies. It matters because stable energy underpins prosperity—disruptions affect billions, from fuel costs to food prices. Policymakers must prioritize de-escalation and reserves to safeguard the future.